AI Infrastructure, Data Centers, and Security Are Now Driving the Tech Market

This week, cloud providers, chipmakers, data center operators, and enterprise software vendors are converging on the same priority: building enough infrastructure to support the rapid rise of generative AI and AI agents. From hyperscale campuses in the United States and Europe to enterprise IT teams planning their next cloud refresh, the pressure is now on GPUs, power delivery, cooling systems, and security controls. The shift matters because AI is moving out of experimental pilots and into production workflows, forcing companies to rethink how they buy compute, move data, and protect critical systems.

Why the AI infrastructure race is intensifying

The current technology cycle is being shaped less by consumer gadget launches and more by the industrial side of computing. Enterprises want faster inference, lower latency, and better control over sensitive data, while cloud platforms are trying to keep pace with demand for model training and AI application hosting. That has created a market in which GPU availability, accelerator efficiency, and cluster design are becoming strategic differentiators rather than behind-the-scenes procurement issues.

Historically, major platform shifts have exposed bottlenecks in the underlying infrastructure. The cloud boom stressed storage and networking. Mobile stressed edge connectivity. AI is doing all of that at once, while also consuming large amounts of power and requiring specialized hardware. The result is a wave of investment in high-density racks, liquid cooling, faster interconnects, and more sophisticated workload orchestration. In many cases, the infrastructure roadmap is now being set as much by energy and real estate constraints as by software ambition.

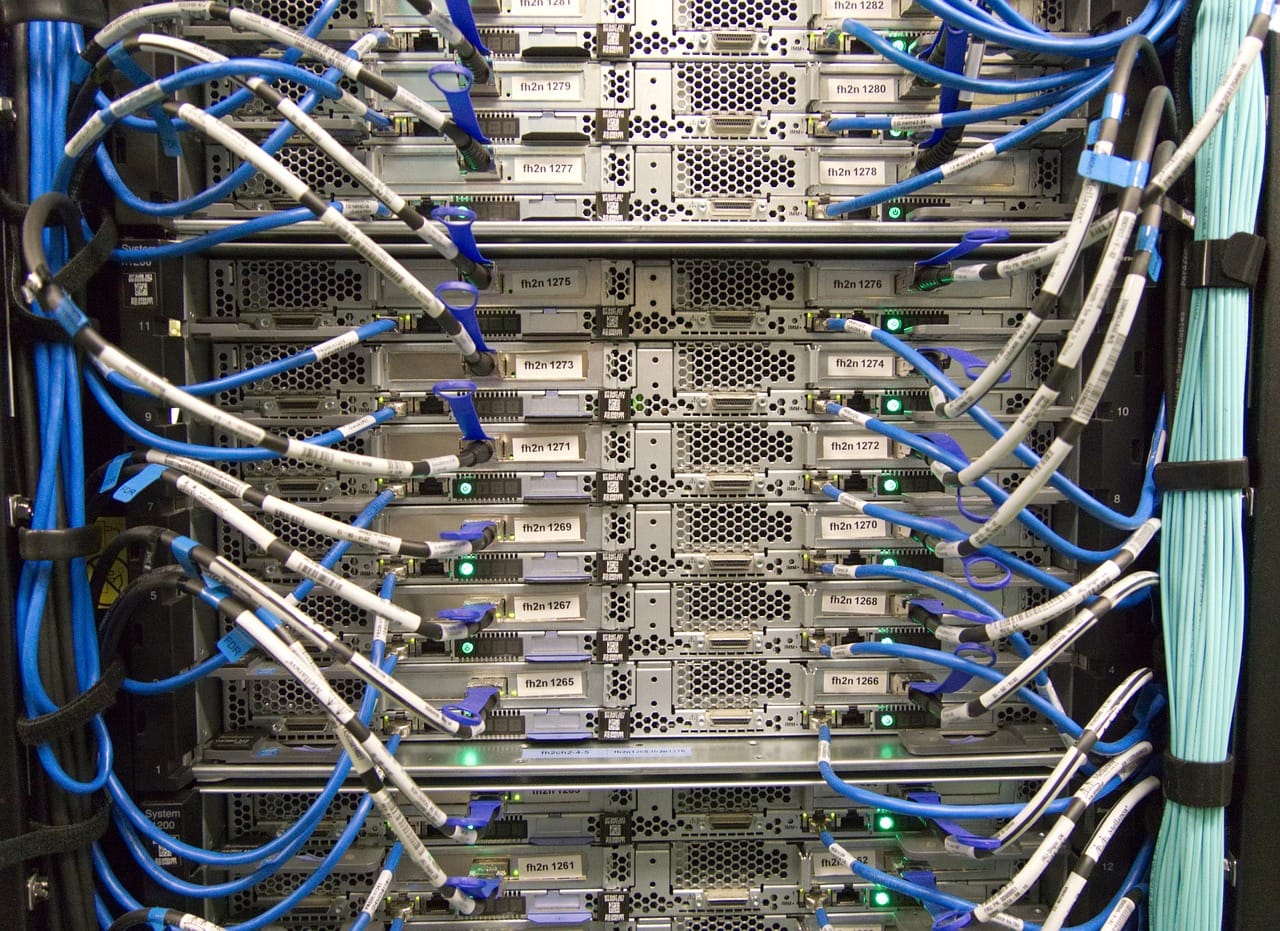

Data centers, power, and networking are becoming the new bottlenecks

One of the clearest trends across infrastructure media and enterprise channels is the growing focus on where AI workloads will physically run. Data center operators are under pressure to support dense GPU clusters that draw far more power per rack than traditional enterprise servers. That is pushing renewed interest in liquid cooling, advanced heat management, and facility upgrades that can handle sustained high loads without sacrificing reliability.

Networking is also moving up the stack. AI workloads depend on fast east-west traffic inside clusters, which is increasing demand for high-throughput Ethernet, low-latency fabrics, and smarter traffic management. Vendors across the ecosystem are positioning for this change with faster switches, better telemetry, and architectures that can keep accelerator pods synchronized. For cloud architects, this means cluster design is no longer only about compute capacity; it is also about how efficiently data can move between GPUs, storage layers, and model-serving endpoints.

Market reactions reflect that reality. Chipmakers benefit when buyers want more accelerators, but they also face pressure from customers who are trying to balance performance, cost, and power use. Cloud providers are expanding managed AI services to reduce friction, while startups are racing to offer tools for inference optimization, model routing, and workload scheduling. The competitive landscape is therefore shifting from simple hardware supply to end-to-end platform control.

Security teams are treating AI as both a tool and a risk surface

Cybersecurity is another reason this trend is accelerating now. As organizations deploy generative AI into customer support, software development, and internal knowledge systems, they are also introducing new attack surfaces. Prompt injection, data leakage, identity abuse, and model supply chain risk are now part of the security conversation. That is changing how CISOs evaluate AI vendors and how engineering teams design guardrails around sensitive workflows.

Recent industry discussion has shown a growing preference for private inference environments, tighter access controls, and clearer auditability. Security teams want visibility into what data is being sent to models, where it is stored, and how outputs are being used downstream. For software developers, this is leading to more demand for policy enforcement, content filtering, and retrieval-augmented generation architectures that reduce the need to expose raw corporate data to external systems.

This is also where enterprise buyers are becoming more selective. Many companies are no longer asking whether to use AI, but how to do so without creating compliance or operational risk. That means vendors with strong governance features, data residency controls, and identity integration are gaining an edge. In practical terms, AI adoption is increasingly tied to the maturity of the surrounding security stack.

What enterprises, investors, and vendors are watching next

The next phase of the market will likely be defined by efficiency rather than novelty. Enterprises are looking for AI systems that can deliver useful results at lower cost, which is driving interest in model optimization, smaller domain-specific models, and hybrid deployments that combine cloud and on-premises resources. CIOs and CTOs are also under pressure to justify AI spend with measurable productivity gains, especially as infrastructure bills rise.

Investors and startups are paying close attention to the infrastructure layer because it often reveals where durable value will accumulate. Companies that improve accelerator utilization, reduce networking overhead, or simplify AI deployment may benefit even if they are not building foundation models themselves. Meanwhile, telecom providers and data center operators are adapting to new demand patterns that favor high-capacity connectivity, edge readiness, and faster provisioning.

The broader industry implication is clear: AI is no longer just a software story. It is an infrastructure story, a security story, and increasingly a power story. Over the coming months, watch for more investment in liquid-cooled facilities, stronger AI governance tooling, wider deployment of inference-optimized systems, and continued competition among cloud and chip vendors to own the enterprise AI stack. The biggest risk is that demand will keep outpacing supply, forcing companies to make harder tradeoffs between speed, cost, resilience, and control.

Frequently Asked Questions

Why is AI infrastructure becoming a bigger market driver than AI software itself right now?

Because many AI projects are moving from trials into production, the limiting factor is no longer just model quality. Companies now need enough GPUs, power, cooling, and networking to run those models reliably at scale. That shifts value toward the infrastructure layer, where availability, efficiency, and deployment speed can decide who can actually deliver AI services.

Why are data centers suddenly so central to AI strategy?

AI workloads are much denser than traditional enterprise applications, so they demand far more power per rack and generate more heat. That makes data center location, electrical capacity, and cooling design strategic issues rather than facilities details. For many operators, the question is now whether the building can support the workload at all.

What makes networking more important for AI clusters than it was for ordinary cloud workloads?

AI systems often move huge amounts of data between GPUs during training and inference, so internal cluster traffic becomes a bottleneck very quickly. Low-latency fabrics, high-throughput Ethernet, and better traffic orchestration help keep accelerators synchronized. In practice, a fast chip is less useful if the network cannot feed it efficiently.

What are the security risks that make enterprise AI deployments more complicated?

Generative AI introduces new ways for attackers to manipulate systems or extract information. Common concerns include prompt injection, accidental data leakage, identity abuse, and risks from third-party model components. Because these threats can affect both the model and the surrounding workflow, security teams are treating AI as a new attack surface, not just a new application.

Why are companies increasingly choosing private inference environments instead of public AI services?

Private inference gives organizations more control over sensitive data, access policies, and audit trails. That matters when AI is used in customer support, internal knowledge search, or software development, where confidential information may be involved. It also helps reduce exposure to external dependencies and makes it easier to apply enterprise-grade guardrails.